Data for this article is based on this article by Ben Dwyer: https://www.cardfellow.com/blog/interchange-fee/

When you accept credit cards, you then need to use a credit card processing interchange.

The Interchange company that you use will have fees that then become a cost associated with credit card processing. These costs and are established by the card brands (Visa, MasterCard, Discover) of open-loop processing systems.

Visa states that “the primary role of interchange is to create an equitable balance of incentives between a cardholder’s financial institution — which issues Visa cards to consumers — and a retailer’s financial institution that enrolls retailers and processes Visa transactions for them.”

When a credit card transaction takes place the issuing bank (cardholder’s bank) pays the acquiring bank (merchant bank) for their cardholder’s purchase less the interchange fee for the transaction. The acquiring bank (merchant bank) then pays their merchant from the remaining balance minus a markup for processing the transaction.

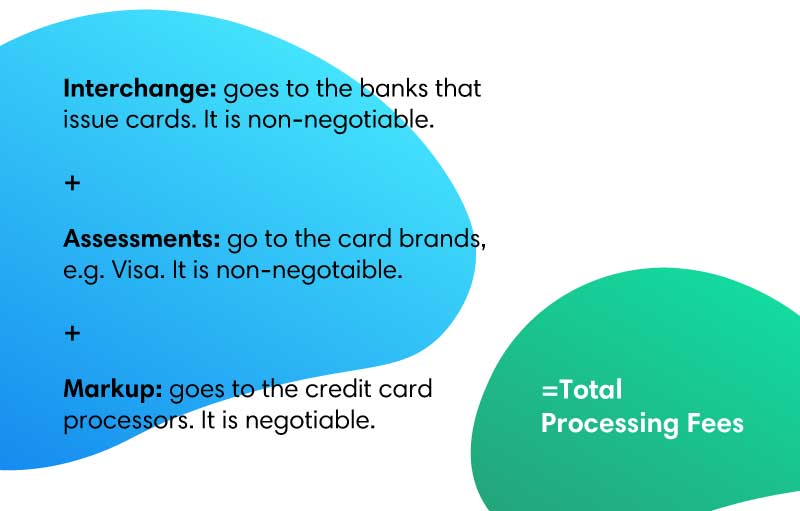

Merchants ultimately receive the gross amount of the sale minus a series of base costs and markups that include interchange, dues, assessments and the processor’s markup. These fees are described in more detail in this article from CardFellow written by Ben Dwyer: https://www.cardfellow.com/blog/credit-card-processing-fees/

Interchange fees for the two largest card brands may change twice annually, in April and October.

Interchange Qualification

The portion of a transaction that’s taken by an issuing bank for interchange depends on the interchange category that the transaction falls under as dictated by the card brand (Visa, MasterCard). The process of categorizing a transaction is called interchange qualification, and it happens on a per-transaction basis.

A few factors are used to determine where a transaction qualifies at interchange. Some of these factors can be controlled or influenced by the merchant while others can’t. Factors that merchants can influence include:

Processing method

Card-present and card-not-present are the terms used to generally refer to the different ways of processing a credit card transaction. Card-present interchange categories carry smaller fees than card-not-present categories.

- Card-Present: Card-present transactions are those where a merchant can read a customer’s credit card data electronically. This process is referred to as electronic data capture.

- Card-Not-Present: In the case of a card-not-present transaction the cardholder’s information is entered manually by the merchant or provided by the cardholder through a gateway or portal.

Transaction data

The information supplied with a credit card transaction impacts how it qualifies at interchange. Proper and complete transaction data is especially important for merchants that process card-not-present transactions and for those that deal with corporate and government enhanced data.

Merchant Category Code

Specific interchange categories exist for businesses that fall under a certain merchant category code (MCC) designations.

Interchange qualification factors that a merchant can’t control include:

- Card Type: Separate interchange categories exist for credit and debit card charges.

- Card Brand: The brand of a bankcard will impact interchange qualification. This criterion is typically associated with credit cards that yield some type of reward for the cardholder.

- Card Owner: Whether a credit or debit card is issued to an individual, business, corporation or municipal agency impacts interchange qualification.

Interchange Optimization

Interchange fees account for the majority of a business’s credit card processing expense, making it very important to ensure that most transactions qualify to the lowest possible categories as often as possible. The process of adapting a business’s processing behavior to achieve the lowest possible interchange costs is called interchange optimization.

The extent to which interchange can be optimized for your business depends on several variables and is a question that you should address with your merchant service provider.